![crypto[native]](https://substackcdn.com/image/fetch/$s_!baju!,w_120,h_120,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fc94827b0-d403-4ff4-a1dc-b507623bbbd2_1000x1000.png)

Designing an AI-Native Trading System

How Seneca uses dynamic state transitions, risk controls, and structural safeguards to navigate crypto volatility.

TL;DR: Most trading strategies do not fail because their signals are wrong. They fail because they cannot survive being wrong long enough to eventually be right. The Seneca Prime Composite has produced strong risk-adjusted performance since inception, including a 6.84 Calmar Ratio, 3.70 Sharpe Ratio, and -17.39% maximum drawdown at full 4x leverage, while maintaining near-zero beta to BTC (0.01) and minimal correlation (0.05). The driver behind these results is what we call the Risk Shield, a capital protection architecture embedded inside Seneca, our AI-native Intelligence Engine of Markets that dynamically manages exposure across changing market regimes.

If you want the deeper breakdown of how this architecture works, you can read the full explanation here:

READ THE FULL ARTICLE ON NAUTILUS BLOG

Performance First, Explanation Second

Over the past year, the Seneca Prime Composite strategy has produced results that attract attention quickly. Metrics such as Sharpe and Calmar ratios are often the first numbers allocators look at when evaluating systematic strategies, and in that context the performance has been strong.

However, when people ask what drives those results, the conversation almost always turns immediately toward signals. They want to understand what indicators the system tracks, how the models forecast price movement, or what predictive features the AI uses to identify opportunities.

Signals are only part of the story.

Most trading strategies do not fail because their signals are wrong. Markets are inherently uncertain systems, and even strong predictive models experience extended periods where outcomes deviate from expectations. Strategies fail when they lack the structural ability to survive those moments. When volatility expands, liquidity disappears, or momentum reverses faster than expected, poorly designed systems exhaust their capital before their edge has time to reassert itself.

This insight shaped much of the architecture behind Seneca, the AI-native asset management platform we have been developing at Nautilus Labs.

Markets rarely move in a straight line. Periods of strong momentum are often followed by abrupt reversals, sideways consolidation, or sudden volatility spikes that can quickly erode gains for strategies that are not built to adapt. One of the core ideas behind Seneca is that performance in crypto markets depends not only on signal quality, but on how well a system can navigate these shifting regimes in real time. If you want a deeper look at how Seneca identifies and adapts to changing market conditions, including the role of regime detection and dynamic positioning across assets like ETH, SOL, and BTC, you can read the full breakdown here:

Navigating Noise: How Seneca Outperforms in Shifting Crypto Regimes

The Rise of AI-Native Asset Management

Traditional quantitative strategies often rely on relatively static rule sets. Entry conditions are defined in advance, exit conditions are predetermined, and position sizing follows fixed portfolio formulas. These approaches can perform well during stable conditions, but they often struggle when markets transition into unfamiliar regimes.

AI-native asset management systems approach the problem differently. Instead of treating trades as static decisions, they continuously evaluate the state of each open position in real time. Momentum, liquidity conditions, position size, and price behavior are constantly reassessed, allowing the system to adapt as market conditions evolve.

The conceptual shift may sound subtle, but it fundamentally changes how risk is managed. Rather than asking only whether a trade should be entered or exited, the system continually evaluates what state the position currently occupies and what action that state requires. Exposure can increase, decrease, or harvest profits incrementally depending on how the environment changes.

Seneca was designed around this philosophy from the beginning. At its core, the platform operates as a Finite State Machine that evaluates every open position tick by tick and transitions between operational states depending on real time market conditions.

Risk management therefore becomes an embedded structural component of the strategy itself rather than a separate overlay applied after the fact. The architecture that governs this process is what we call the Risk Shield.

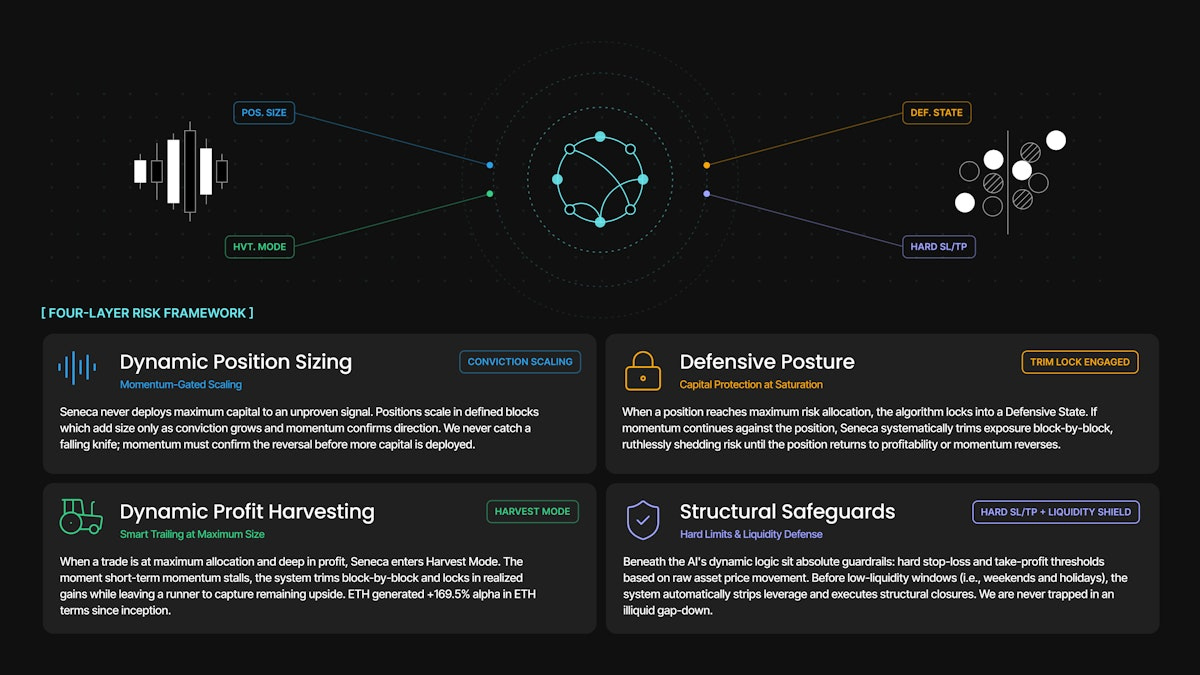

The Four Layers of the Risk Shield

The Risk Shield operates as a four-layer capital protection architecture that governs how exposure enters and exits positions as market conditions evolve.

The first layer is dynamic position sizing. Rather than deploying maximum capital to an unproven signal, Seneca scales into trades incrementally using predefined blocks. Additional capital is deployed only when momentum confirms the direction of the position. If the market temporarily moves against the strategy, the system only averages down once reversal momentum is confirmed, which avoids the classic mistake of attempting to catch falling knives.

The second layer is defensive posture, internally referred to as Trim Lock. When a position reaches maximum allocation and momentum begins moving against it, the system transitions into a defensive state. Exposure is then reduced gradually as the algorithm sheds blocks one at a time until the position stabilizes or exits entirely. Removing human discretion from this process helps prevent one of the most common behavioral mistakes in trading, which is doubling down on losing positions.

The third layer governs profit harvesting. When a position reaches full allocation and remains profitable, Seneca enters what we call Harvest Mode. Instead of waiting for a full reversal to exit the trade, the system trims exposure incrementally as short term momentum begins to stall. This locks in realized gains while leaving a portion of the position active so it can continue capturing additional upside.

The fourth layer consists of structural safeguards that operate beneath the dynamic decision logic. These include hard stop loss and take profit thresholds tied directly to asset price movement rather than leverage levels. The system also accounts for liquidity conditions by automatically reducing leverage ahead of known low liquidity windows such as weekends and holidays. This prevents the strategy from being trapped in sudden illiquid price gaps.

Together these mechanisms form a coordinated framework that continuously adapts exposure based on real time market conditions.

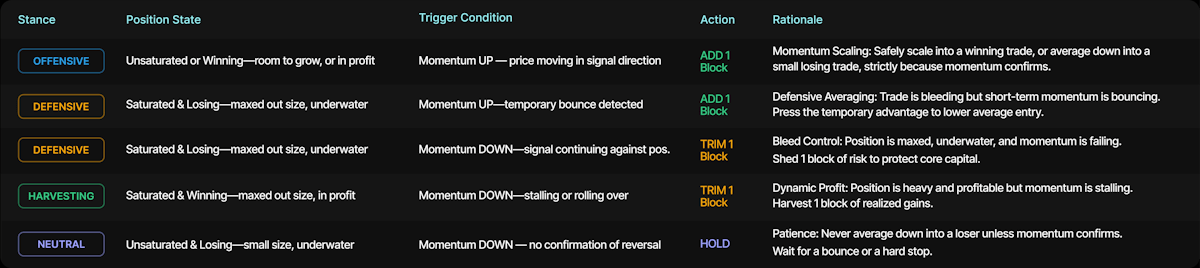

The State Machine Behind the System

Behind the Risk Shield sits the state machine that governs how positions transition between operational modes.

Every open position exists within a defined state determined by its size, profitability, and the direction of momentum. As those variables change, the system transitions between states and applies the rule set associated with that state. A position gaining momentum may scale into larger exposure, while a max sized position losing momentum may transition immediately into defensive trimming.

Because these transitions are deterministic, decisions are executed instantly without discretionary overrides or human latency. The system observes the state of the position, applies the relevant rule, and executes the action in real time.

This structure allows Seneca to continuously adapt to changing market regimes without relying on static assumptions about how prices should behave.

Understanding the architecture of a strategy is important, but real confidence comes from observing how a system performs under live market conditions over extended periods of time. Seneca has now accumulated thousands of hours of live trading across multiple market regimes, providing a growing dataset that helps us evaluate how the system behaves when volatility expands, liquidity shifts, or momentum regimes change.

For readers interested in the operational side of building and validating an AI-native trading engine, we recently published a deeper look at what we have learned from that process and how live market exposure has shaped the evolution of the platform. You can read the full article here:

The Nautilus Edge: 6,300 Hours of Live Trading

Survivability Is the Real Edge

The broader lesson extends beyond any single strategy.

Markets are becoming faster, more fragmented, and increasingly driven by automated systems. In that environment the advantage is shifting toward AI-native asset management platforms that can dynamically adapt to changing conditions rather than relying on rigid portfolio rules.

Prediction alone is not enough to sustain performance over long periods of time. The systems that endure are not necessarily the ones that forecast the future most accurately. They are the ones that are structurally capable of navigating uncertainty while preserving capital.

The Risk Shield was designed around that principle. Its purpose is not to ensure that every trade is correct, which is impossible for any strategy. Instead it ensures that when trades are wrong, losses remain controlled and capital remains available for the next opportunity.

In markets, survivability is not simply a defensive objective. It is the foundation that allows compounding to occur over time.